Zero-Depreciation Car Insurance Explained: Benefits, Limitations, Claim Rules and Whether It's Worth It

Buying car insurance is the easy part. Understanding what your policy will actually pay out when your car is damaged - that's where most owners get caught off guard.

A damaged bumper, headlamp, mirror or body panel needs replacing. Most owners assume the insurer foots the entire bill. Under a standard comprehensive policy, that's rarely true - the insurer deducts an amount for the part's depreciation before settling the claim, leaving the owner to cover the gap. That's the problem zero-depreciation cover - "zero-dep" - is built to solve. Here's all that you need to know about the zero dep insurance.

Quick Summary

What it does | Waives or reduces the depreciation deduction on eligible replaced parts during a claim |

What it doesn't do | Cover wear and tear, mechanical breakdown, or turn insurance into a maintenance plan |

Best for | New cars, premium/EV owners, city drivers, first-time owners |

Typical age limit | Up to 5 years (some insurers extend to 7) |

Claim limits | Usually capped - often 1-2 claims/year on entry plans |

What Is Zero-Depreciation Car Insurance?

Zero-dep is an add-on bought alongside a comprehensive or own-damage policy - it doesn't exist on its own. It targets one specific gap in standard cover: depreciation on replaced parts.

A normal policy assumes vehicle parts lose value with age and use, so when a part is replaced, the insurer pays out less than its current cost - the owner absorbs the difference. Zero-dep cover has the insurer waive or substantially reduce that deduction, so more of the repair bill is covered.

You may also see it called:

- Zero-dep insurance

- Bumper-to-bumper insurance

- Nil-depreciation cover

- Depreciation waiver cover

Naming varies by insurer, but the underlying benefit is broadly the same.

Why Depreciation Matters in a Claim

Every part loses value over time - plastic and rubber components age faster than metal ones. When an accident damages a part, the insurer factors this loss of value into the payout.

Example: A car's front bumper is damaged in a low-speed collision. Replacement costs Rs. 12,000. Under a standard policy, the insurer deducts depreciation before settling - the owner pays that deducted amount plus the compulsory deductible. With zero-dep, that depreciation deduction is waived, and the owner's out-of-pocket cost drops considerably.

Depreciation by Part Type

Depreciation treatment depends heavily on what the part is made of. Claim calculations vary by insurer, but the broad pattern looks like this:

Part type | Examples | How it's typically depreciated | Zero-dep impact |

|---|---|---|---|

Plastic | Bumpers, grilles, mirror housings, dashboard trims | High deduction - common in minor accidents | Deduction generally waived on eligible parts |

Rubber | Hoses, seals, bushes, wiper blades, door beading | Treated as wear-and-tear; deteriorates with age | Covers accidental damage only, not age-related wear |

Fibre | Body kits, spoilers, premium trims/panels | Prone to cracks; can attract heavy deduction | Especially valuable for fibre-heavy exteriors |

Metal | Doors, bonnet, fenders, roof, boot lid | Depreciated by vehicle age - older car, bigger deduction | Reduces impact, but treatment varies by insurer |

Modern cars lean heavily on plastic and fibre components in bumpers, headlamps and cladding - so even a minor accident can generate an expensive replacement bill.

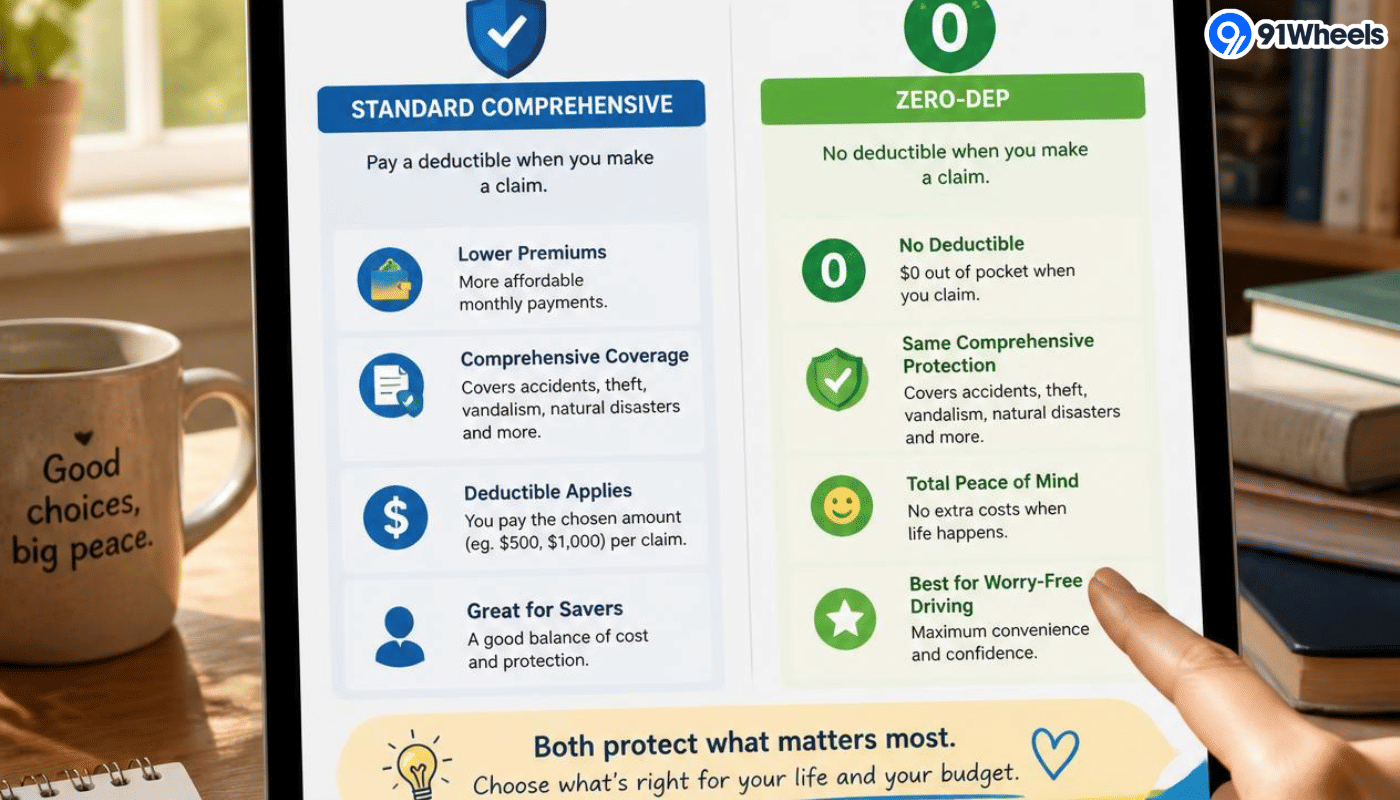

Standard Comprehensive vs Zero-Dep: A Worked Example

A zero-dep policy is essentially a comprehensive policy plus a depreciation waiver. Here's how the numbers can shift:

Repair bill after an accident:

Item | Cost |

|---|---|

Front bumper | ₹15,000 |

Headlamp assembly | ₹18,000 |

Side mirror | ₹8,000 |

Fibre trim and cladding | ₹6,000 |

Labour | ₹7,000 |

Total | ₹54,000 |

- Standard comprehensive policy: Insurer deducts depreciation on the bumper, mirror, trim and other eligible parts. The owner pays several thousand rupees out of pocket, on top of the compulsory deductible.

- Zero-dep policy: Depreciation on eligible parts is waived. The insurer settles a much larger share of the ₹54,000; the owner pays only the compulsory deductible, uncovered consumables, and any exclusions.

The gap widens further when the damage involves multiple plastic, rubber or fibre parts.

What Zero-Dep Covers

Zero-dep helps with depreciation on parts replaced after an insured event - it doesn't cover anything the base policy excludes. Typical scenarios include:

- Accidental collision damage

- Damage caused by another vehicle

- Damage from falling objects

- Natural calamities, where covered

- Fire-related damage, where covered

- Replacement of eligible plastic, rubber, fibre and metal parts

If the underlying claim is invalid - say, the driver had no valid licence - zero-dep won't rescue it. The add-on only kicks in once the base policy has already accepted the claim.

What Zero-Dep Does Not Cover

This is the part buyers most often get wrong. Zero-dep is a depreciation waiver, not a maintenance plan. Common exclusions:

- Normal wear and tear

- Mechanical or electrical breakdown unrelated to an accident

- Engine damage from driving through water after the engine has stalled

- Careless or illegal driving, or driving without a valid licence

- Driving under the influence

- Damage outside the policy's declared geographical area

- Tyre damage, unless it happened in a covered accident

- Battery replacement due to ageing

- Consumables (engine oil, coolant, nuts, bolts) unless separately covered

- Consequential damage from continuing to drive a damaged vehicle

- Claims made after policy expiry

- Unapproved modifications or undeclared accessories

- Routine servicing costs

Example: A car stalls after being driven through deep water, and repeated restart attempts cause engine damage. This is typically treated as consequential damage - zero-dep alone won't cover it. A separate engine protection add-on may be needed, and even then, coverage depends on the specific circumstances.

Are Tyres Covered?

Rarely, and only partially. A tyre damaged in an accident may be covered depending on the policy - but wear, punctures, ageing and sidewall cracks are not. Even where accident-related tyre damage is covered, insurers often pay only a portion of the cost, calculated against tread wear and tyre age. Always check the policy wording specifically for tyre terms rather than assuming zero-dep covers them by default.

Claim Limits and Age Eligibility

Factor | What to expect |

|---|---|

Claims per year | Often capped at 1-2 on standard plans; higher or unlimited plans cost more |

Vehicle age | Readily available up to 5 years; some insurers extend to 7 depending on model and condition |

Premium trend | Rises with vehicle age as claim probability increases |

Before buying, confirm:

- The maximum number of zero-dep claims allowed per year

- Whether there's a separate cap on parts or repair value

- Whether the benefit applies to every claim type or only select ones

- Whether the cover renews after a claim is used

- Whether the insurer adjusts premiums after multiple claims

"Zero depreciation" does not mean unlimited, unconditional repair claims.

How a Zero-Dep Claim Works

The process mirrors a standard comprehensive claim - the difference is only in how the payout is calculated.

- Inform the insurer and register the claim

- Share photos, location and incident details

- Take the car to a network garage for cashless repair, if available

- Allow the insurer's surveyor to inspect the vehicle, if required

- Submit RC, driving licence, policy and claim form

- Receive repair approval once the insurer reviews the estimate

- Pay the compulsory deductible, non-covered items and any exclusions

- Collect the car after repair and settlement

Even with zero-dep, expect to pay for consumables, the compulsory and voluntary deductible, and anything specifically excluded.

Is It Worth Buying?

For most owners in the early years of ownership - yes. Modern cars carry expensive bumpers, LED headlamps, sensors, cameras and painted panels, so even a minor accident can produce a repair bill far above expectations. If one claim saves an amount close to or greater than the add-on's annual cost, it's paid for itself.

It's not automatically essential for everyone, though. The right call depends on the car's age, likely repair costs, driving conditions and how comfortable you are covering repairs yourself.

Good fit for:

- New car buyers - high IDV, costly genuine parts, greater exposure to expensive replacements

- Premium car owners - luxury/SUV models with expensive lighting, sensors and body panels

- EV owners - costly components and specialised repairs, even if batteries aren't fully covered

- City drivers — higher exposure to scrapes, mirror knocks and minor collisions in traffic

- First-time owners - lower out-of-pocket risk on early claims

- Owners of cars with costly exterior parts - large painted bumpers, LEDs, cladding, premium alloys

Less essential for:

- Older cars with low market value

- Cars with inexpensive spare parts

- Vehicles rarely driven

- Owners comfortable self-funding small repairs

- Cars nearing the end of their ownership cycle

- Drivers who prefer to avoid small claims to protect their No Claim Bonus

Zero-Dep vs No Claim Bonus

These two work against each other in small-claim situations. Zero-dep reduces the deduction when you claim; No Claim Bonus rewards you for not claiming.

Example: A Rs. 3,000 bumper scratch might cost less to pay out of pocket than the No Claim Bonus you'd forfeit at renewal by filing a claim. Zero-dep earns its keep on significant repair bills - not on small scratches where the NCB math favours paying yourself.

Checklist Before Buying

- Age limit applicable to your car

- Number of claims allowed per year

- Coverage across plastic, rubber, fibre and metal parts

- Tyre terms - included, limited, or excluded

- Whether consumables are covered

- Whether engine protection needs a separate add-on

- Cashless repair network near you

- Compulsory and voluntary deductible amounts

- Whether your accessories/modifications are declared

- Whether cover is restricted to OEM parts only

The cheapest premium isn't automatically the best deal - broader terms, a strong cashless network and reliable claim support are often worth paying slightly more for.

Final Takeaway

Zero-depreciation insurance addresses a real gap in standard comprehensive cover - the depreciation deducted from replaced parts. It's particularly valuable for new cars, premium vehicles, EVs and city driving, where bumpers, lights, mirrors and body panels take the most hits.

It isn't blanket protection, though. Wear and tear, routine maintenance, most tyre issues and several engine scenarios still fall outside its scope, and claim limits and age eligibility apply. The smartest approach: buy it while the car is new or relatively young, read the exclusions closely, and reserve claims for repairs where the depreciation waiver actually moves the needle - not every minor scratch.

Do you like this article?

Comments

No comments yet. Be the first to comment!